I used to think all advisors got paid the same way.

Turns out I was wrong (and) it cost me.

You’re probably wondering How Do Investment Advisors Get Paid Gscfinanceville. Not in vague terms. Not with jargon.

You want the real answer. The one that affects your account balance.

Most people don’t know how their advisor makes money. They sign paperwork, nod along, and hope for the best. That’s dangerous.

It leads to surprises. Confusion. Mistrust.

If you don’t know how they’re paid, you can’t tell if their advice lines up with your goals. Or theirs.

This guide cuts through the noise. No fluff. No fine print translations.

Just clear, plain-English breakdowns of the three main ways advisors earn money.

You’ll learn which payment method creates conflicts of interest (and which doesn’t). You’ll see how fees actually show up on your statements. And you’ll walk away knowing exactly what to ask before hiring anyone.

This isn’t theory. I’ve sat across from advisors who wouldn’t answer straight questions about their pay. You deserve better.

Read this (and) you’ll stop guessing.

You’ll start knowing.

AUM Fees: The Standard Way Advisors Get Paid

I see this one all the time.

It’s the most common way advisors get paid.

That’s where How Do Investment Advisors Get Paid Gscfinanceville comes in (and) AUM is usually the first answer you’ll hear.

AUM stands for Assets Under Management.

It means they charge a percentage of the total money they manage for you.

Say you have $100,000 invested and the fee is 1%. You pay $1,000 per year. Simple math.

(Though it adds up fast if your portfolio grows.)

Here’s the upside: if your account drops to $75,000, your fee drops too (to) $750. Your advisor also wins when your money grows. That alignment feels fair.

(Most of the time.)

But here’s what no one shouts loud enough: those fees compound against your returns. A 1% fee on $1 million is $10,000 every year. That’s not chump change.

That’s a vacation. Or six months of rent.

You’re paying whether the market goes up or down.

And small percentages hide big dollars over time.

Want to dig into how that stacks up against flat-fee or hourly models? Check out Gscfinanceville. It breaks down real numbers (no) fluff.

Commission-Based Payments: What They Are

I’m not sure why this isn’t explained up front.

But commission-based advisors get paid when you buy or sell something (not) for watching your money grow.

They earn a cut on mutual funds. Annuities. Insurance policies.

Stocks. Bonds. That’s it.

One payment. One time. Per trade.

You don’t pay them monthly. You pay them then. And that “then” happens every time you move money into one of those products.

Here’s what bugs me: that setup creates pressure. An advisor might push a high-commission annuity. Even if a low-cost index fund fits you better.

They’re not evil. They’re just paid to sell.

You’re the one who owns the risk.

Not them.

So ask: Did you recommend this because it helps me (or) because it pays you?

If they hesitate, that’s your answer.

This is part of How Do Investment Advisors Get Paid Gscfinanceville. Some charge fees. Some take commissions.

Some do both. None of it is illegal. But all of it matters.

You’ll see the fee on your statement.

It won’t say “this is why I picked it.”

It’ll just say “$249.99.”

That’s fine (if) you knew before you clicked. Most people don’t. I didn’t (until) my first annuity surrender charge hit.

(Ouch.)

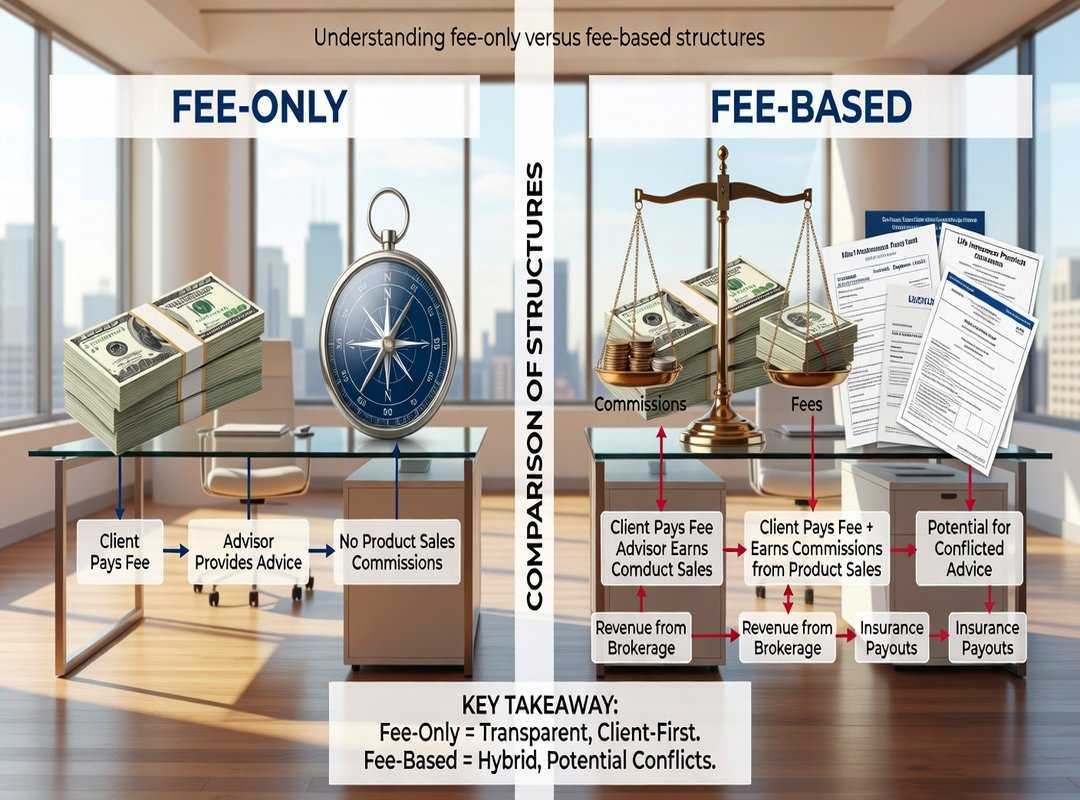

Fee-Only vs. Fee-Based: Know Who’s Really on Your Side

Fee-Only means the advisor gets paid only by you. No commissions. No kickbacks.

Just your fee. Usually a percentage of assets or an hourly rate.

That’s it.

Fee-Based sounds similar but it’s not. They can charge you a fee and take commissions from products they sell you. Like mutual funds or insurance policies.

Why does that matter?

Because now their income ties to what they recommend (not) just what works for you.

You’re already wondering: What did they push me into last year? Was it best (or) just profitable for them?

Ask this straight up: “Do you earn any commission on anything you recommend?”

If they hesitate, or say “it depends,” walk away.

This distinction isn’t small print.

It’s the difference between advice and sales.

How Do Investment Advisors Get Paid Gscfinanceville?

Start by reading the fine print (and) then head to Where Can I Find Financial Advice Gscfinanceville to see real options near you.

Don’t assume. Ask. Then decide.

Pay by the Hour or the Job

I paid an advisor $225 an hour to review my 401(k) choices. It took 90 minutes. I got a list of three funds to switch into.

Done.

Hourly rates work like a lawyer’s bill. You pay for time, not assets. You ask questions.

They answer. You stop when you’re done. No ongoing commitment.

No AUM minimums.

Fixed fees are different. You pay one price for one thing. Like $1,800 for a full retirement plan.

Or $950 for estate documents. The advisor doesn’t care if you have $5,000 or $500,000. The job is the same.

These models suit people who don’t need hand-holding every quarter. Or those whose portfolio is small but their questions are real. Why pay 1% of $30,000 a year just to get basic advice?

You’re not buying a relationship. You’re buying expertise on demand. That’s it.

How Do Investment Advisors Get Paid Gscfinanceville? Some charge by the hour. Some charge by the job.

Others still take a cut of your portfolio. But that’s not the only way. And honestly?

It’s often not the fairest one.

You want help with taxes next month? Pay for next month. Not for the next ten years.

How Do Investment Advisors Get Paid Gscfinanceville

Ask Before You Trust

I’ve watched people hand over their life savings (then) get blindsided by hidden fees. You’re not dumb for being confused. The system is built to confuse you.

How Do Investment Advisors Get Paid Gscfinanceville

That question alone separates the transparent advisors from the rest.

You deserve to know exactly how your advisor makes money.

Not “generally.” Not “in broad terms.”

Exactly.

Fee-only? Fee-based? Commission-based?

Each model pushes different behavior. And some push sales, not advice. You already know that.

You’ve felt it.

So ask:

How are you compensated?

Are you fee-only, fee-based, or commission-based?

What are all the fees I will pay. Directly and indirectly?

Are there conflicts of interest I should know about?

Don’t settle for vague answers. Walk away if they hesitate. There are other advisors.

Better ones.

You came here because you’re tired of guessing. Tired of surprise fees eating your returns. Tired of trusting someone who won’t answer straight.

So do this now:

Pick one advisor you’re considering. Email them those four questions. Wait for the reply.

If it’s not clear, concise, and upfront. Move on.

Your money isn’t a test drive. It’s yours. Protect it like it is.

Editorial Director

Editorial Director